The Start of a REVOLUT-ion? (Financials Unshackled Going Deep Edition 1, Issue 5)

Revolut has received approval to launch its UK bank - so what?

The material below does NOT constitute investment research or advice and is for informational and educational purposes only - please scroll to the end of this publication for the full Disclaimer

Revolut has more than 65 million customers globally…yet the average customer keeps just c.£400 in their account…that’s the paradox at the heart of the most valuable fintech in Europe…but yesterday’s UK banking licence may finally change that

Welcome to Financials Unshackled Going Deep. With yesterday’s news that the UK Prudential Regulation Authority (PRA) has lifted restrictions on Revolut’s banking licence following a successful mobilisation period and given its approval for Revolut to launch its UK bank, I want to share some perspectives on this important development and provide an updated view on its banking business more broadly.

Key Take-Aways

The UK licence is a major credibility milestone for Revolut.

Revolut still has extremely low deposit intensity relative to incumbents.

The key strategic question is whether the licence translates into trust and primary account status.

If it does, the UK could become the first proof-of-concept for Revolut’s global banking model - while its activities in other markets develop in parallel.

There is a potential ‘twist’ in the longer-term. While a key focus over the coming years will likely be on building trust and primary account relationships - the traditional playbook - the AI era may bring the final decoupling of banking between the front end (relationships) and the back end (balance sheet capability). Revolut, which seems likely to continue to build out its wider product and service capabilities in parallel with its banking push, is playing for the former while traditional banks are still structurally anchored to the latter.

Approval received to launch UK bank

A strategic inflection point?

This is, in my view, a hugely significant development and a landmark moment in Revolut’s journey. This is the first banking licence issued to Revolut in a G7 or a developed world country with the exception of Lithuania (Revolut uses the Lithuanian licence to operate Revolut Bank UAB across the EEA under passporting rules) in my understanding. Before I flesh out why I see this as such a landmark moment in Revolut’s journey, let’s consider the shape of its banking business today. If you are familiar with some of my recent writings you can skip on to the ‘Is the UK bank licence a game-changer?’ section.

Shape of its banking business today

SYNTHESIS: Revolut has achieved extraordinary scale in customer acquisition, but its balance sheet remains extremely shallow relative to traditional banks.

Revolut has made great strides

Revolut’s traction from a customer acquisition perspective is undeniably impressive. The company has already surpassed 65 million customers globally and is targeting 100 million by mid-2027*. Its latest funding round implied an equity valuation of $75bn and a recent Bloomberg article here notes that investors have been pushing for a further share sale process later this year that would value the business at $100bn at least (ahead of a potential listing for which a valuation of at lest $150bn is targeted, according to the same Bloomberg article) - a materially higher number than the market cap of the large cap UK domestic-focused banks, Barclays (BARC), Lloyds Banking Group (LLOY), and NatWest Group (NWG). Revolut is much more than just a bank and generates substantial revenues from services like cryptocurrency, for example. However, given the fresh licence approval relates to its banking services (Revolut has previously been authorised as an investment firm in the UK, etc.), the focus of this note is on its business in a fractional reserve banking context. Indeed, I would also add that my strong view is that the latest valuation of Revolut and its shareholders’ ambitions for future valuations bake in an assumption that it will succeed in breaking into mainstream banking markets.

* Note that Revolut’s UK customer base stood at 11 million in 2025 when it noted that its total customer base surpassed 65 million globally. Yesterday’s press release here noted that its UK customer base is now 13 million so it seems likely to me that its global customer base exceeds 70 million by now.

Average deposits are very low vs. traditional banks

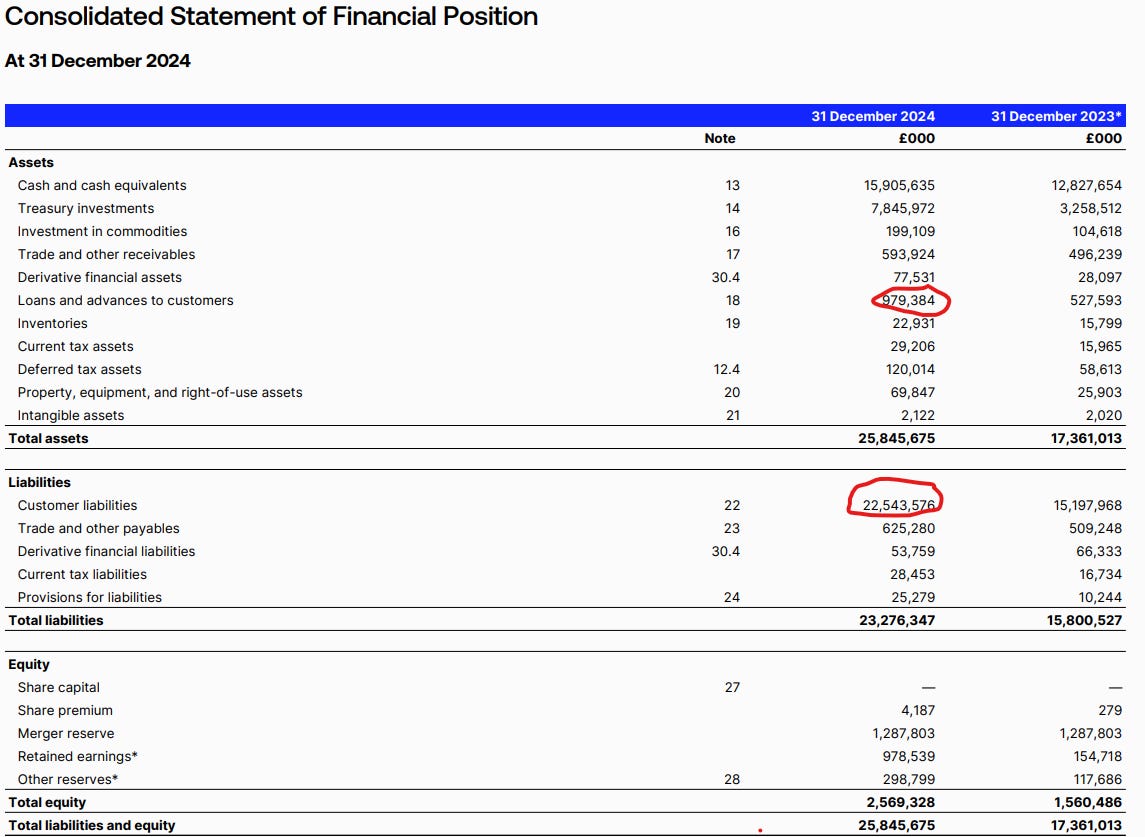

Revolut is not a publicly listed firm and we have to rely on quite old financial information until its 2025 accounts are published. The firm reported deposits of £22.5bn at the end of 2024. That implies an average balance of slightly more than £400 per account, including its business customers. For some context, its average balances at that date equated to just c.2% of the average balances at LLOY and NWG – and a significantly smaller percentage of the average balances at AIB Group (AIBG) and Bank of Ireland Group (BIRG) on my calculations. However, an important caveat is that its 13 million UK customers comprise more than one-sixth of Revolut’s entire customer base so, given that the firm did not then have a UK banking licence, it seems reasonable to conclude that its stock of deposits and average deposit balances per customer are meaningfully suppressed. Still though, given how light its average balances are relative to traditional incumbents of size, there is clearly a mountain to climb.

Why don’t depositors place more money with Revolut?

In my view it is a question of trust and I wrote about this last October in Business Post here. While customers routinely use Revolut for instant payments and FX transfers they appear far less eager to use it as a primary bank account into which their wages and salaries are paid. This is a systemic challenge for any aspiring newcomer disruptor. I have written here and here about Starling and Monzo’s struggles to sustain meaningful low-cost deposit build despite the fact that their combined total deposits are still just a small fraction of the UK deposit market at less than £30bn. Starling’s deposits stood at just £12.1bn at the end of March 2025 – representing a growth rate of 10.0% y/y but: i) off a very low base relatively speaking; and ii) likely bolstered by the fact that Starling increased rates paid on its current accounts in the year. Monzo reported deposits of £16.6bn at the same date, which were +48% y/y - massively overshadowing the 10% growth in deposits achieved by Starling in the same period - but this growth was supported by instant access balance build, which come at a price and it was notable that Monzo’s deposit interest expense charge almost doubled in the year. Let’s not forget that these two have been around for a long time now.

Indeed, Revolut has received significant negative publicity in relation to customer service and fraud. The BBC Panorama documentary in 2024 shone a light on this as have statistics from Which? showing Revolut experienced the highest number of fraud and scam complaints escalated to the UK’s Financial Ombudsman Service in 2024 - and again in the 8 months to August 2025. Regular articles documenting customer troubles frequently appear in the Irish media, which is unsurprising given the platform’s penetration in that market. Indeed, the Irish Independent reported in December 2025 here that a business customer Paul Walsh reported a breach and was greatly dissatisfied with the service he received, noting: “I had to go to the gardaí, the Financial Services and Pensions Ombudsman, the Central Bank of Ireland, multiple solicitors and independent cyber-security experts, just to get help…The security of your money and basic customer service should be fundamental components of any bank”.

Revolut has been addressing challenges

Revolut has stated it takes fraud very seriously, maintaining that it has “robust controls” to meet its legal and regulatory obligations – and rejects Walsh’s arguments, with a spokesperson reportedly remarking to the Irish Independent: “Revolut has full confidence that its customers’ accounts and funds are wholly protected and goes to every length to support users who report fraud”. Still, the regular cycle of negative publicity is hardly constructive for building the trust required to be a primary bank. Revolut has indeed been making efforts in recent years to ‘tidy up’ its corporate structure and controls, including the appointment of Martin Gilbert as Group Chair and Francesca Carlesi as UK CEO. Carlesi herself has noted that three key focus areas are: i) building trust; ii) broadening the product range; and iii) strengthening security and safety capabilities. This demonstrates recognition of the challenge – but trust is a hard battle to win.

Lending is in its infancy

From a lending standpoint, Revolut is only in its infancy. By the end of 2024, less than £1bn of customer deposits had been recycled into loans, as can be seen from the below extract from Revolut’s 2024 Annual Report. Let’s remember that this is a business with global disruption ambitions. Its intended foray into Irish mortgage lending has been delayed though, anecdotally, I hear that the business is having considerable success with its Irish personal loans product. Nevertheless, volumes here are likely negligible in an overall Irish market lending originations context.

The long-term is a different question

As I have written before, none of this is to say that Revolut can’t succeed in the longer-term. The theory is that a low-cost, highly scalable model can drive competitive advantage from an operating leverage perspective relative to the incumbents – with slicker technology underpinning a far superior customer proposition. But, first, Revolut must acquire sufficient customer deposits. Trust is not easily won. Meanwhile, traditional UK incumbents like LLOY and NWG are actively delivering significant advancements in their customer propositions and strengthening their efficiency, thereby narrowing the competitive gap. And, to the extent that Revolut does become a meaningful player in deposit markets, it must then prove it can recycle those funds to consistently generate sustainable adequate risk-adjusted lending margins through the cycle. That’s a monumental undertaking - but that doesn’t mean it can’t be done.

Is the UK bank licence a game-changer?

I believe it could be

I think it could turn out to be quite the inflection point that Revolut management has been working towards for years - marking the beginning of a meaningful momentum shift in Revolut’s relationships with its customer base globally, not just in the UK. This will only become evident with the passage of time of course. But what is so significant about the UK licence approval is that the UK is Revolut’s home market and it marks the first full banking licence that it has attained in a developed economy with the exception of Lithuania. I had become more sceptical over time that the business would ever ‘get there’ in the UK - but yesterday’s news puts paid to that doubt.

Why? One word: Trust

The granting of a UK bank licence will not build customer trust in and of itself. Revolut has been ‘tidying itself up’ as I noted above but appears to still have a long road to travel in this vein - however, management appears determined to continue on this journey. But acquiring a licence in the highly developed UK market constitutes a significant seal of approval for its culture, its governance, its risk controls, and, perhaps most importantly, in a broader model validation context - in a way that customers in the UK and many other developed markets don’t necessarily associate with the Lithuanian licence that the firm uses to passport into other European banking markets. And, given its multi-jurisdictional presence and global ambitions, its status as a trusted bank can become cemented over time through that international recognition - which is a much tougher ask for neobanks with a presence in just one or a few countries (so, using Monzo’s and Starling’s average deposits in the UK as readacross for Revolut’s capability, for example, may lead to deeply erroneous conclusions - and, while we’re on the comparability point, even though Monzo has global banking ambitions, Revolut is miles ahead given it has been busy acquiring customers across many geographies for many years). Trust build would be constructive for the development of primary account relationships.

Indeed, Revolut’s global ambitions look likely to accelerate now that it has attained a UK bank licence given that this should pave the way for regulators elsewhere to build on the BoE’s assessment - with press reports late last year indicating that regulators in the US, Australia, New Zealand, and Switzerland have reportedly told Revolut executives they would like to see the UK licence granted before signing off their own licence approvals. No surprise now that Revolut filed an application with the OCC in the US earlier this month.

Proving out its model in the UK will be a key priority

Revolut will undoubtedly now focus intensively on building out its UK capability, seeking to unlock its 13 million customer base in that geography. Yesterday’s press release indicates that this has already been mapped out. Revolut’s Co-Founder and CEO Nik Storonksy noted in the press release that Revolut looks forward “to introducing a full suite of banking services to our millions of UK customers” and UK CEO Francesca Carlesi’s remarks built on this, noting that “Securing this licence lays the foundation for our next chapter: expanding into a broader suite of products, including credit, to sit alongside the innovative services our customers already rely on every day. This will now enable us to continue on our mission to deliver the most seamless, secure, and customer-centric banking experience for consumers across the UK.” Indeed, the main body of the press release noted that it “…will gradually begin the process of rolling out current accounts to new customers in a few days, starting with a small group and expanding over the coming weeks to ensure a smooth user experience”. But Revolut has, arguably, already proven that it has the management bandwidth to give the UK the focus it needs while, in parallel, continuing to target new licences and growth across multiple overseas regions.

This is not an overnight journey - but the foundations for long-term success are there

From a UK perspective, the first step is building out its deposits franchise - getting to an adequate average deposit balance per customer, which is the key metric to watch going forward in my view. This will undoubtedly take some time. Revolut has struggled in other markets in this respect (e.g., Ireland, Spain) though those markets are characterised by elevated customer inertia, with the UK a more fluid market for deposit-gathering. That said, Monzo and Starling have struggled so this is no fait accompli. But even though Monzo is a household name in the UK with better brand recognition than Revolut (according to Statista and Kantar data), Revolut has been catching up fast in terms of customer numbers and looks set to outflank Monzo very soon if its current pace of growth continues. And Revolut’s international penetration and recognition gives it an edge over Monzo in my view in terms of prospective customer conversion to primary account user. But it will have to execute clinically and that is by no means guaranteed.

The deposits hold the key to proving concept in a banking context as I see it but that’s not to underestimate the scale of the challenge in developing a lending business that can churn out adequate risk-adjusted returns on equity through-the-cycle. UK lending initiatives will lag the deposits push (which is set to start within days as noted above) but will in due course, essentially, happen in parallel. The language in Revolut’s press release - such as ‘gradual’, ‘discipline’, and ‘long-term’ - is instructive and shows more maturity than yesteryear (though the BoE may have made its views known on what should be said!). Developing out a lending business will take time as Revolut is essentially nowhere in this respect at the current time. However, preparations have been underway in other markets at least - for example, mortgages - and, while there have been delays (e.g., Ireland mortgages), I suspect the business will ‘get there’ eventually.

Ultimately, I still see this as very much a long-term journey - consistent with comments I have made before around the potential for this business to succeed in the long-term. However, the attainment of the UK licence increases my confidence that the destination can be achieved (even if, as some sceptics have suggested, the BoE felt under pressure from government to grant Revolut the licence). But, right now, Revolut has not ‘proven concept’ in a fractional reserve banking context and the monumental undertaking to grow into what is an enormous valuation (though not solely related to banking activities it must be said) by: i) becoming a significant player in deposit markets in multiple jurisdictions; and ii) proving it can recycle those funds to consistently generate sustainable adequate risk-adjusted lending margins through-the-cycle. But that’s not to say it can’t be done.

Trust build as a next step but unlikely to be ‘the end game’

Indeed, there is something of a potential ‘twist’ here as I see it. While I believe that, looking through the lens of how to compete with traditional banks over the coming years, it is essential for Revolut to build with its customers the trust that is needed for them to become comfortable using the bank as their primary account, driving associated deposit capture. That seems the likely medium-term playbook. AI could accelerate that journey. For example, if real-time deposits migration (as I have written about for many years) ever becomes a reality (interesting article in The Financial Brand here on Monday), the barrier for primary accounts could collapse - but AML and other related regulatory obstacles prevail for now. Thinking further on this, in an AI-intermediated world, it is arguably direct customer ownership that becomes the ‘holy grail’. But while trust will be a prerequisite, in the long-term customer ownership isn’t necessarily going to be where the commodity deposits sit. In the AI era, we are potentially going to see the final decoupling of banking between the front end (relationships) and the back end (balance sheet capability) - Revolut is clearly playing for the former while traditional banks are still structurally anchored to the latter. Whose interface the customer uses to talk to the AI may be the decisive factor. Revolut has shown its prowess in this vein already - evidenced by its customer penetration, leveraging its many products and services (beyond just banking). As customer interfaces sophisticate one would be churlish to discount Revolut’s ability to play ahead of the game. Indeed, if Revolut can use AI to own the interface where financial decisions are made, they may not need to wait for traditional cycles to prove their model. I feel we are still a good number of years away from this eventuality to the extent it ever manifests - but that might suit Revolut too. Time will tell.

Closing Note

Please note that this newsletter is one of a three-part Financials Unshackled Newsletters product suite. The other newsletters are: i) Financials Unshackled Ireland (and Europe) Weekly Essentials & Perspectives (sent via own email on Sundays; click here for the latest one); and ii) Financials Unshackled UK Weekly Essentials & Perspectives (sent via own email on Sundays; click here for the latest one). Further product refinements are planned for mid-April and I’ll share details in due course. Thanks for being part of this growing community and email me at john.cronin@seapointinsights.com / DM me in the app if you want to give any feedback or if you want me to add you to the other Newsletter distribution lists (just write Y in reply to this mail).

⚠️ Disclaimer ⚠️

The contents of this newsletter and the materials above (“communication”) do NOT constitute investment advice or investment research and the author is not an investment advisor. All content in this communication and correspondence from its author is for informational and educational purposes only and is not in any circumstance, whether express or implied, intended to be investment advice, legal advice or advice of any other nature and should not be relied upon as such. Please carry out your own research and due diligence and take specific investment advice and relevant legal advice about your circumstances before taking any action.

Additionally, please note that while the author has taken due care to ensure the factual accuracy of all content within this publication, errors and omissions may arise. To the extent that the author becomes aware of any errors and/or omissions he will endeavour to amend the online publication without undue delay, which may, at the author’s discretion, include clarification / correction in relation to any such amendment.

Finally, for clarity purposes, communications from Seapoint Insights Limited (SeaPoint Insights) do NOT constitute investment advice or investment research or advice of any nature – and the company is not engaged in the provision of investment advice or investment research or advice of any nature.

Great piece as always John.. One thought on the deposit question: I wonder if the answer is simpler than it looks. Revolut's user base skews heavily young, over 70% between 18 and 34. These aren't typically people sitting on meaningful savings balances. If your core user has £800 spread across all their accounts, no amount of great UX is going to move the needle on deposits.

The low deposit volumes may be less about product design or trust and more about customer economics. They just don't have much to deposit. Enormous user numbers, low per-customer value